The Covid-19 pandemic has served as a catalyst for the co-working sector and many corporates are now eager for flexible workspaces which can accommodate inconsistent occupancy numbers and cut real estate costs. We’ve seen clearly that many of the workforce now prefers to work hybridly, and the co-working sector has jumped in to fill this demand.

Co-working had been seen as a space primarily for smaller companies to save on real estate by renting shared, contemporary office spaces. Now, more and more big corporations are jumping on board. The workforce are demanding spaces that provide comfort, freedom, and choice, and the co-working sector is determined to deliver. Many co-working companies have used technology to manage their growth and manage their buildings better.

Covid-19: The Great Gamechanger

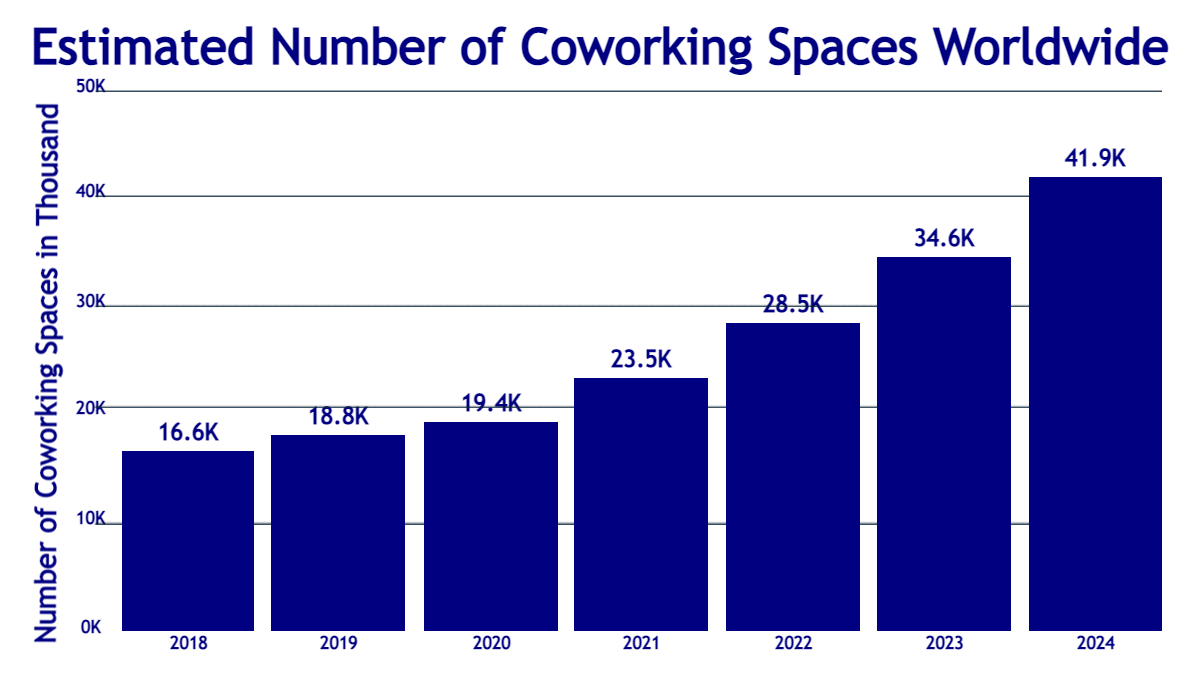

There are currently an estimated 19,500 co-working spaces globally, and that number is growing rapidly, and is projected to more than double to 40,000 by 2024. The co-working sector is now worth $16.1 billion, and the market’s worth is expected to soar to over $30 billion by 2026. The sector is extremely hot, with 87% of co-working spaces now profitable. That’s 50% higher than in 2021. Of those, 63% of co-working providers see profit margins of over 15%.

Seeing the Growth in Green

With this stark growth in spaces and profits, it’s natural that the eyes of big corporations are turning towards co-working as an efficient and lucrative option in times of such uncertainty. Just this year, there have been a series of large investments in co-working companies by some of the world’s largest corporates. In May, one of co-working’s most prominent companies, Industrious, saw an extra $100 million in investment from CBRE, adding to the $220 million already invested by them. Industrious also acquired two large international co-working operations – Asia’s Great Room Offices and Europe’s Welkin & Meraki – for $100 million. With investments and acquisitions such as these becoming more commonplace, co-working companies are swiftly becoming some of the leaders in commercial real estate.

In a similar vein, some of the most technically advanced co-working companies The Office Group and Fora announced in March a £1.5 billion merger backed by Blackstone. This will see both companies acquiring a combined 3.1 million square feet of office space stretched across mainly the south of England. The two companies are also looking to spread further into Europe to become the premiere providers of co-working office space throughout the continent.

Rapid Change from a Corporate Point of View

The effects of co-working and hybrid operations are also changing how some of the biggest global corporations are growing. Just last week, retail goliath Amazon announced that they were pausing construction of six planned office towers. The towers, one of which has already been completed at 20-storeys and 566k square feet, were set to be built in both Tennessee and Washington state, but changes to floor-plans to accommodate for hybrid-working have caused construction to be halted indefinitely. The expectations of many employees to have the option to work remotely or in a hybrid fashion has dramatically shifted how buildings managers, constructors, and FM staff have to consider how their offices function and what is financially viable in this new hybrid environment.

The Branding Dilemma

Like much of what has sprung out of the pandemic, figuring out the ideal implementation of a hybrid workspace is a work in progress. As it stands, the flex office has a bit of an image problem, a problem that overpromises and under delivers. After a pandemic that saw office buildings suffering from dramatically decreased occupancy levels and the surging energy prices that came alongside that, co-working spaces are trying a lot of tricks to get people back into the office. However, for many, the ping-pong tables, free beer, and movie nights are not much more than a gimmick.

The branding of these co-working spaces, and who they want to attract as target occupants, is a vital part of the hybrid equation. For some, the playful atmosphere of adult jungle gyms is what catches the eye, for others, a more traditional office space is desired. Some are prioritising the social aspects of the workspace that the pandemic took away, such as communal areas and cafes, whereas others are more focused on spaces for individual solitude. Ultimately, co-working companies have a delicate balance to strike, and have to make decisions on who the most beneficial customer to market to is.

Keeping Energy Down: Occupancy and Beyond

What makes the flex office such a promising sign for a wavering workforce is its ability to provide accurate occupancy data, so buildings and companies know exactly what they’re using and who they’re using it on.

There are innovative technologies that deliver occupancy and efficiency solutions. To start, co-working spaces often benefit from hot-desking, wherein an employee can occupy a specific desk through a booking system on a rolling basis, meaning that the space is utilised correctly and not wasted if they don’t come in to work. There are a variety of companies that provide this kind of space management software, with the highest ranked being Nexudus, with 100% of users stating they are likely to renew their subscription.

On top of this, buildings can implement occupancy sensors, which paint a clear picture of how many people are inside a building, down to a granular level. Occupancy rates can be seen for individual floors or zones of large buildings, meaning that what energy is being used can be efficiently measured and managed. Sensors like these can be particularly game changing for the co-working sector, enabling them to understand how they can vary membership types to maximise occupancy and minimise costs to tenants.

It’s Time to Expand

It’s no understatement that Covid-19 was a devastating time for both the co-working and commercial real estate sectors, but it also presented an unique opportunity for change. The world’s work culture mutated, and it’s going to stay altered for a long while yet. The way buildings are managed has to change with it. As we see ourselves in the heart of a devastating climate crisis and see energy prices shoot through the roof, it’s no longer acceptable to shrug off the wasted energy and stick our heads in the sand. Co-working spaces, and those who manage them, need to carry on leading the way with efficient space utilisation delivered through sensors and software.

Share your thoughts

No Comments

Sorry, the comment form is closed at this time.